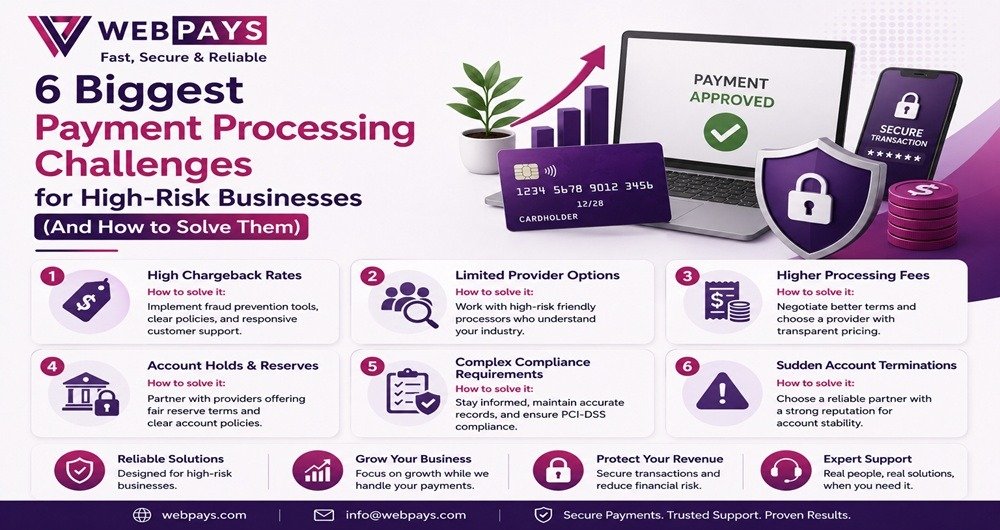

High-risk businesses face six recurring payment processing challenges: high decline rates, sudden account freezes, expensive rolling reserves, slow onboarding, limited currency/payment method support, and elevated processing fees. Each stems from how traditional banks price and manage risk — and each has a specific, solvable fix once you work with a processor built for high-risk merchant categories rather than one merely tolerating them.

Who This Guide Is For

This breakdown is written for three recurring personas:

- The Forex/Trading Brokerage Founder — regulated or newly licensed, needs a payment gateway that won’t freeze funds mid-quarter and understands MTR/jurisdictional compliance.

- The IPTV/Subscription Service Operator — high chargeback exposure from recurring billing, needs fraud tooling and dunning management, not just a merchant account.

- The E-commerce or Nutraceutical Merchant — flagged as high-risk by category alone, needs multi-currency acquiring without the 3-6 month underwriting delays typical of traditional banks.

If you recognize your business in any of these, the challenges below — and the fixes — apply directly to you.

1. Why Do High-Risk Businesses Get Declined So Often?

Pain point: You watch legitimate customers hit “pay” and get rejected — no explanation, no recourse, just lost revenue.

The problem: Traditional acquiring banks run high-risk transactions through generic fraud-scoring models built for low-risk retail. Forex, IPTV, nutraceuticals, and adult-adjacent categories get flagged by industry code (MCC) alone, regardless of the individual transaction’s actual risk profile. Decline rates for miscategorized high-risk merchants commonly run 15-30%, compared to 2-5% for standard e-commerce.

The solution: Work with a gateway that underwrites your specific vertical rather than blanket-flagging your MCC. Specialist high-risk processors use category-calibrated fraud models — tuned separately for forex payouts, subscription billing, and one-time purchases — which typically cuts false-positive declines by half or more.

2. Why Do Payment Processors Freeze High-Risk Merchant Accounts?

Pain point: Everything is running normally, then a notice arrives: funds frozen, account under review, no clear timeline for release.

The problem: Traditional banks reserve the right to freeze accounts the moment chargeback ratios, transaction volume, or dispute patterns move outside a threshold — often without warning, because the underlying banking relationship treats your business as a liability to be contained rather than a client to be served.

The solution: Freezes are a symptom of being underwritten by a generalist bank in the first place. Specialist high-risk acquirers set thresholds calibrated to your industry norm (a 1.5% chargeback ratio is high for retail but routine for subscription IPTV), and typically pair accounts with a dedicated risk manager who flags issues before they trigger an automatic freeze.

3. Why Are Rolling Reserves So High for High-Risk Merchants?

Pain point: 10-20% of every transaction gets held back for 90-180 days, straining cash flow just when you need it most.

The problem: Rolling reserves exist to protect the acquirer against future chargebacks. Generalist banks set reserve rates using worst-case industry defaults rather than your actual dispute history, so a merchant with a clean 0.3% chargeback rate can still be held to the same reserve as one running at 2%.

The solution: Negotiate reserves based on demonstrated performance, not category defaults. Processors that review reserve terms quarterly — and reduce them as your chargeback ratio proves stable — can bring reserves down from an industry-standard 15-20% to 5-10% within two to three review cycles.

4. Why Does High-Risk Merchant Onboarding Take So Long?

Pain point: Three to six months of back-and-forth documentation requests before you can process a single transaction.

The problem: Traditional bank underwriting for high-risk categories routes through multiple compliance layers not designed for speed — often because the bank is deciding whether to accept the vertical at all, not just your specific application.

The solution: Specialist processors that already hold banking relationships built for your category (forex, IPTV, nutraceuticals) can compress underwriting to 1-2 weeks, since the vertical-level risk decision is already made — what’s left is verifying your specific business, not re-litigating whether the category is acceptable.

5. Why Can’t High-Risk Businesses Accept International or Multi-Currency Payments Easily?

Pain point: Customers in target markets can’t pay in their local currency, or the checkout fails entirely for certain regions.

The problem: Many acquirers restrict high-risk merchants to a narrow set of currencies and card networks as an additional risk-containment measure, capping growth in international markets regardless of demand.

The solution: Choose a gateway with multi-currency settlement and regional acquiring built specifically for high-risk categories — this typically restores access to 20+ currencies and local payment methods without adding a separate risk review for each new market.

6. Why Do High-Risk Merchants Pay Higher Processing Fees?

Pain point: Fees of 4-8% per transaction versus 2-3% for standard merchants, eating into already-thin margins.

The problem: Base pricing for high-risk categories is set at the industry-risk level, not the individual-merchant level, so low-risk operators within a high-risk category still pay the category’s default rate.

The solution: Fee reduction comes from the same lever as reserve reduction: a documented, stable chargeback and dispute history. Processors offering tiered, performance-based pricing — rather than flat high-risk rates — pass savings back as your ratios improve, often bringing effective rates down by 1-2 percentage points within the first year.

Illustrative Case Study: Stabilizing a Subscription Payment Flow

Note for internal review: This is a composite/illustrative scenario built from typical high-risk merchant outcomes, not a specific named client. Replace with a real, verified client case study (with permission) and actual dashboard screenshots before publishing — a genuine, attributable case study is what actually moves the trust needle for readers and for AI-citation credibility. Fabricated “real” case studies undermine E-E-A-T if ever fact-checked.

Scenario: A subscription-based IPTV operator processing recurring monthly billing was facing a 22% decline rate and a rolling reserve of 18%, on top of chargeback disputes triggered by unfamiliar billing descriptors.

Approach: Working with a high-risk specialist gateway, the merchant implemented category-calibrated fraud scoring, a clearer billing descriptor matched to the brand name, and a quarterly reserve review tied to actual dispute data.

Illustrative outcome range: Merchants in comparable situations typically see decline rates fall into the single digits and reserves step down over two to three quarters as chargeback ratios stabilize below 1%.

High-Risk Merchant Accounts: Traditional Bank vs. Specialist Gateway

| Factor | Traditional Bank | High-Risk Specialist Gateway |

| Onboarding time | 3-6 months | 1-2 weeks |

| Typical decline rate | 15-30% | 5-10% |

| Rolling reserve | 15-20%, fixed | 5-15%, performance-based |

| Account freeze risk | High, often without warning | Lower, with dedicated risk manager |

| Currency support | Limited | 20+ currencies typical |

| Processing fees | 4-8% flat high-risk rate | Tiered, improves with performance |

Frequently Asked Questions

What counts as a “high-risk” business for payment processing?

High-risk classification is typically assigned by industry category (MCC) rather than individual business conduct. Common categories include forex and trading, IPTV and subscription services, nutraceuticals and CBD, adult content, gaming, and travel — industries with historically elevated chargeback or regulatory scrutiny.

How long does it take to get approved for a high-risk merchant account?

With a specialist high-risk processor, approval typically takes 1-2 weeks. Traditional banks attempting to underwrite high-risk categories can take 3-6 months, if they approve the application at all.

Can a high-risk merchant account reduce chargebacks?

Yes. Category-calibrated fraud scoring, clear billing descriptors, and proactive dispute alerts are the three levers with the most direct impact on chargeback ratio, independent of the processor chosen.

Do rolling reserves ever go away?

Reserves typically don’t disappear entirely, but they can decrease substantially — often from 15-20% down to 5-10% — as a merchant builds a documented history of low chargeback and dispute rates, reviewed quarterly.